· The RealXM Team · Home Buying · 5 min read

How a Buyer Cashback Can Expand the Price Range You Can Actually Afford to Close

Most buyers calculate their maximum purchase price based on their mortgage approval. Few factor in closing costs — and almost none factor in a buyer cashback before making an offer. Here's why that calculation order matters.

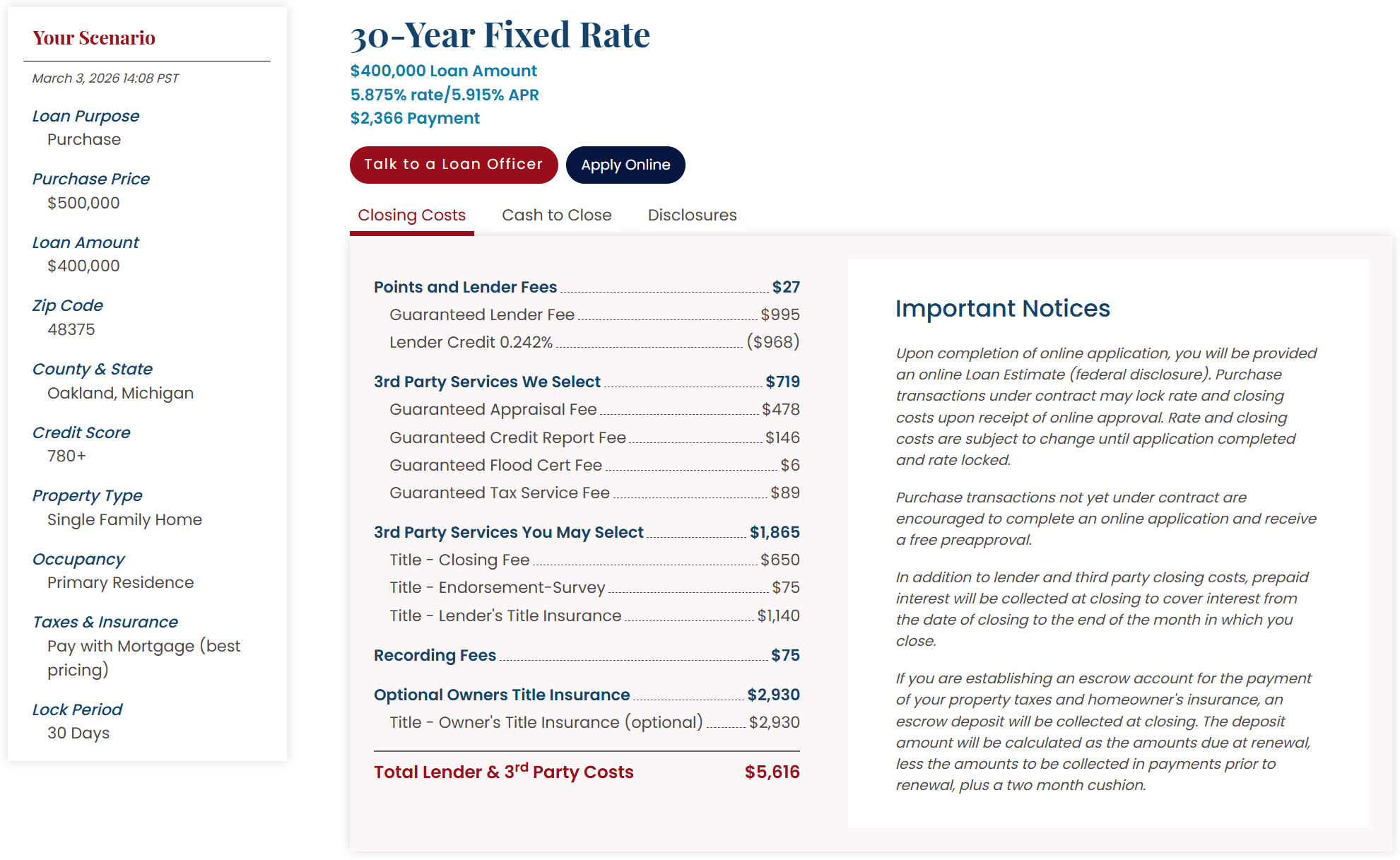

Getting pre-approved for a mortgage answers one question: what monthly payment can you qualify for? It does not answer the question most first-time buyers discover too late — how much cash do you need at the closing table?

For many buyers, that gap between pre-approval and actual purchasing power is where deals fall apart. And it’s also where a buyer cashback, calculated upfront before making an offer, can meaningfully expand the price range a buyer can realistically close on.

The Cash Gap Nobody Plans For

Consider a buyer with $32,000 in savings who gets pre-approved up to $430,000. They plan to put 5% down, which on a $415,000 home would be $20,750. That leaves $11,250 for closing costs.

The problem: closing costs on a $415,000 purchase — including loan origination, title insurance, appraisal, prepaid taxes and insurance for escrow, and recording fees — typically run between $9,500 and $13,000 depending on location and loan type. At $11,000, this buyer has $250 left over after closing. No emergency fund. No buffer for the first month of ownership.

Most financial advisors recommend keeping at least 1–2% of the home’s value in reserve after closing. On a $415,000 home, that’s $4,150 to $8,300.

This buyer cannot responsibly close at $415,000. Their effective ceiling — factoring in closing costs and a minimal reserve — is closer to $385,000.

That’s a $30,000 gap between what the lender says they can borrow and what they can actually afford to close.

Factoring the Cashback In Before Making an Offer

Here’s the shift in thinking that changes the math: a buyer cashback isn’t something that happens to you at closing. It’s a known number you can calculate before you ever make an offer.

If a buyer’s agent offers a 1.5% cashback, and the purchase price is $415,000, the credit at closing is $6,225. That credit reduces the cash the buyer needs to bring to the table — applied against closing costs directly on the Closing Disclosure.

With that cashback factored in before the offer is written:

| Without Cashback | With 1.5% Cashback | |

|---|---|---|

| Purchase price | $415,000 | $415,000 |

| Down payment (5%) | $20,750 | $20,750 |

| Closing costs (est.) | $11,000 | $11,000 |

| Buyer cashback credit | — | −$6,225 |

| Cash needed at closing | $31,750 | $25,525 |

| Savings remaining | $250 | $6,475 |

At $31,750 needed, this buyer cannot close. At $25,525 needed, they close with a reasonable reserve intact.

The cashback didn’t make the deal slightly better. It made the deal possible.

How This Widens the Effective Buying Range

The more useful way to think about a buyer cashback isn’t as a closing cost credit on a specific home — it’s as a structural adjustment to the price range you can actually close on.

For a buyer with $32,000 in savings, putting 5% down, needing $10,500 in closing costs, and wanting $5,000 in post-closing reserves:

Without a cashback: Total cash needed = down payment + closing costs + reserve At a price of X: 0.05X + $10,500 + $5,000 ≤ $32,000 → 0.05X ≤ $16,500 → Maximum purchase price: $330,000

With a 1.5% cashback: The cashback reduces effective cash needed: 0.05X + $10,500 + $5,000 − 0.015X ≤ $32,000 → 0.035X ≤ $16,500 → Maximum purchase price: $471,000

The cashback expands this buyer’s realistic price ceiling by over $140,000 — not because they borrowed more or saved more, but because they factored a known credit into the calculation before searching.

Why This Calculation Belongs Before the Home Search

Most buyers approach home shopping in this order:

- Get pre-approved

- Find homes at the top of the approval range

- Make an offer

- Receive closing cost estimate

- Discover the cash gap

The buyer cashback, if known upfront, belongs at step one — not step four. A buyer who knows they’ll receive a 1.5% credit can set a realistic search ceiling that accounts for the full picture: down payment, closing costs, reserve, and the cashback that reduces the net cash required.

This also changes the offer strategy. A buyer who has already confirmed their agent’s cashback terms can make offers at prices that would otherwise be outside their cash reach — confidently, with documentation ready for the lender, rather than discovering the math problem after an offer is accepted.

What Lenders Need to Know

Buyer cashbacks applied toward closing costs are permitted under standard loan guidelines, including conventional (Fannie Mae/Freddie Mac) and FHA loans. A few practical points:

- The cashback must be documented in the buyer’s agency agreement before closing — not arranged informally after the fact

- Lenders cap total credits based on loan-to-value ratio; in most standard purchase scenarios a 1–1.5% cashback fits within the allowable limit

- The lender will review the cashback as part of final underwriting; inform your loan officer early so there are no surprises

- In some cases, if the cashback exceeds allowable closing cost credits, the excess may be returned as cash or applied to reduce the loan principal, depending on loan type and state

The key practical step: tell your lender about the cashback at the same time you tell them your down payment amount. It’s the same category of information — cash you have available to close.

A Practical Reference by Price Point

For a buyer putting 5% down, with a 1.5% cashback, here is how the net cash requirement shifts across common price points:

| Purchase Price | Down (5%) | Est. Closing Costs | Cashback (1.5%) | Net Cash to Close |

|---|---|---|---|---|

| $300,000 | $15,000 | $8,000 | −$4,500 | $18,500 |

| $375,000 | $18,750 | $9,500 | −$5,625 | $22,625 |

| $425,000 | $21,250 | $10,500 | −$6,375 | $25,375 |

| $500,000 | $25,000 | $12,000 | −$7,500 | $29,500 |

| $600,000 | $30,000 | $13,500 | −$9,000 | $34,500 |

The cashback consistently covers a substantial portion of closing costs — turning a cash-constrained buyer into one who can close with reserves intact.

The Right Time to Ask About Cashback

The right time is before you start your home search — not after you find a home.

Ask any buyer’s agent you’re considering: “Do you offer a buyer cashback, and can we document the terms before I start making offers?” A cashback agent will confirm the amount, explain how it appears at closing, and coordinate with your lender so the credit is properly accounted for in your financing.

That one conversation, held at the start of the process rather than the end, can determine not just how much you save — but which homes are actually within your reach.